01

Understanding the Current State of Agentic AI in Enterprises

Agentic AI at the enterprise level has moved from a demo in early 2024 to production capability by mid-2025, and to a permanent budget line by 2026. The interesting thing is that the entire transition happened in just 24 months. The charts that follow trace the year-over-year ramp and the business functions it has landed in.

Survey Question #1: Does your organization currently use Agentic AI in at least one business function?

We Found that Agentic AI Adoption is Now Near-Universal

The rapid growth of Agentic AI since its launch reveals that enterprises are rapidly shifting from passive tools to autonomous software. Back in 2024, early adoption stood at 28%, but these early agentic frameworks were highly restricted. They mostly operated behind the scenes, handling predictable, single-turn backend automations with heavy human oversight. By 2025, that baseline climbed to 45% as the technology matured. This growth was driven by the integration of LLMs, enabling agents to handle complex, multi-step workflows and interact more naturally across enterprise systems.

By May 2026, adoption had crossed a major operational tipping point, reaching 70%. During our survey, the majority of senior leaders said ‘yes’ to using Agentic AI in at least one business function. Because the threshold has now crossed the 50% benchmark, autonomous agents have become a competitive advantage for early adopters.

‘Yes’ % of leaders who are using AI agents in ≥1 business function

Insight to Capture

The inflection between 2024 and 2026 marks the tipping point for Agentic AI. Its adoption has nearly doubled due to increased awareness, availability, ease of use, and cost-optimized pricing.

AI is Deepest in Customer-Facing and Engineering Functions

Our findings indicate another significant trend toward lateral expansion within surveyed organizations. 3 main reasons for its mass adoption:

- First is intuitive natural-language interfaces that reduce technical barriers to entry.

- Second, these systems connect natively to existing enterprise software and databases, reducing the need for capital and time-intensive legacy infrastructure overhauls.

- Ultimately, cost efficiency is achieved by enabling the organization to reduce marginal cost and operational effort for subsequent departments once its foundational model architecture and security guardrails are established.

To quantify where these autonomous agents generate the highest business value, respondents were asked to map their usage of Agentic AI across their business functions.

Survey Question #2: In which of the following business functions does your organization currently deploy AI Agents?

Here is what we found:

-

Software Engineering (78%): Every 3 out of 4 companies are aggressively shifting from prompt-based AI pilot to autonomous coding agents across the entire SDLC.

-

Customer Support (60%): Enterprises are transitioning to fully agentic resolution systems to navigate backend databases to process refunds, verify identities, and modify reservations without human intervention.

-

New Product Development (55%): Agentic frameworks are being used to accelerate R&D, ingest vast consumer data streams, predict market trends, and instantly generate product formulation hypotheses.

-

Marketing and Sales (43%): Most B2B organizations are deploying agents to eliminate manual pipeline management, generate multi-channel outreach, and maintain CRM accuracy.

-

IT Operations (33%): Cloud-forward Fortune 500 enterprises utilize AI Agents to maintain systemic uptime within their DevOps pipelines to monitor multi-cloud infrastructure, cross-reference telemetry with internal runbooks, and auto-remediate server failures.

-

Manufacturing (9%): Autonomous agents are being used in heavy manufacturing environments despite high physical friction to manage assembly-line telemetry and dynamically re-route supply chains.

Insight to Caption

The top three functions are all revenue- or customer-touching, but software engineering's #1 placement understates its dominance.

02

Mapping Agentic AI Maturity Disparities and Industry-Wise Deployment Footprints

A binary assessment of whether an organization utilizes an agent in a single business function fails to capture the true depth of market penetration. The enterprise ecosystem is divided between organizations that have successfully moved Agentic AI into production and those still navigating the friction of early-stage pilots. This divergence is heavily dictated by industry verticalization.

Tech-savvy organizations with mature data pipelines are rapidly decoupling operational velocity from human headcount, while capital-intensive or safety-critical industries proceed with a measured, compliance-driven approach. To map the true velocity of this transition, this chapter debunks who has moved from pilot to production and which industries are leading.

While Adoption is Universal, Scaling is Not

Let’s begin by breaking down Agentic AI maturity across 6 distinct stages. It maps where organizations actually stand on their journey toward Agentic AI maturity.

Survey Question #3: What is the current maturity stage of AI Agent deployment in your organization?

Industry-Wise Breakdown of Agentic AI Deployments Tells a Different Story

Our cross-industry analysis showed that the ability to scale AI Agents depends on several maturity factors, including operating environment, data readiness, compliance requirements, and tolerance for software-related risk.

To understand how Agentic AI maturity looks in practice, we examined adoption patterns within individual industries. The following deep dives map the production workflows and deployment footprints across four core industries.

1. Tech and Engineering Organizations

While surveying 435 tech organizations within our pool, we found that rather than relying on Agentic AI for isolated tasks, engineering teams are deploying it across the entire SDLC.

Survey Question #4: In which development functions are AI Agents currently deployed in production or active pilot?

Functional Profile of AI Agent Deployment (Multi-Select, N=435)

-

Code Generation (81%): This represents the most mature operation. Field data confirms that agents are widely trusted to ingest functional specifications or engineering tickets and generate production-grade code.

-

Code Review and Bug Fixing (64%): Organizations are increasingly trusting agents with deep contextual access to repositories. These systems parse PRs and diffs against broader system architecture, isolate logical defects, and autogenerate targeted patches.

-

Performance Optimization (64%): Tied for the second-highest deployment rate, this reflects a shift toward automated efficiency. Agents operate within strict guardrails, profile production workloads, and apply code adjustments without human intervention.

-

Testing and QA Automation (58%): This marks a clear transition from rigid, manual testing to dynamic quality assurance. Agents in this segment independently generate test cases directly from raw product requirements and load runs, triage failures, and log structured bug reports.

-

DevOps (57%): This metric highlights the rise of self-healing infrastructure. AI agents actively monitor CI/CD pipelines and runtime environments to mitigate system downtime and debug routine pipeline blockages.

-

Technical Documentation (52%): Engineering teams are deploying agents to permanently solve documentation drift. By continuously monitoring the active codebase, agents dynamically update API docs, generate changelogs, and synchronize technical modifications to internal repositories.

-

Security Analysis / SAST/DAST (42%): This function currently shows the lowest deployment rate. However, as per our assessment, this reflects strict corporate risk compliance rather than a lack of capability. Entrusting an agent to scan runtime traffic and self-patch security flaws requires a high level of organizational trust. As automated verification frameworks mature, this specific deployment footprint is poised for the sharpest acceleration over the next fiscal cycle.

2. Healthcare

Our discussion with senior executives at over 365 healthcare enterprises indicated that they adopt a highly risk-stratified approach when embedding autonomous AI Agents into their workflows. The deployment densities reveal a systematic progression in which organizations establish high-trust baselines in low-risk operational environments before scaling agentic autonomy to experimental clinical decision-support systems.

To understand the operational scope of these parallel implementations, we mapped the exact clinical and functional areas driving active healthcare deployment.

Survey Question #5: Which functions does your organization currently maintain active Agentic AI deployments for?

-

Administrative Automation (58%): It is the primary maturity benchmark, in which organizations have successfully deployed agents to navigate the entire revenue cycle from initial code extraction to autonomous denial remediation.

-

Patient Engagement and Chatbots (43%): Our team observed a major shift toward automated remote care coordination. Healthcare institutions are now trusting agents to manage the interface among patient logistics, post-visit instructions, and provider routing.

-

Drug Discovery and R&D (38%): We also observed that life sciences enterprises are utilizing AI Agents as self-directed computational engines to compress early-stage laboratory timelines through autonomous molecular modeling.

-

Personalized Treatment Planning (28%): This restrained adoption is a clear indicator of institutional hesitation. While Agentic AI is technically mature enough to aggregate data and cross-reference guidelines, findings show that leadership remains fundamentally uncomfortable letting algorithms synthesize care pathways without exhaustive, physician-in-the-loop oversight.

-

Telemedicine Triage (18%): This compressed footprint reflects defensive risk management. The enterprises remain cautious where AI output directly influences care access and urgency decisions.

3. Manufacturing

Within the manufacturing industry, the Agentic AI shift is governed by the realities of physical operations. Because changing physical production lines requires significant time and software integration, market adoption scales differently depending on workflow complexity.

Our data from 320 surveyed manufacturing organizations shows that manufacturers are prioritizing areas where AI Agents can be deployed quickly within existing software systems to drive immediate efficiency gains. By rolling out these parallel implementations, enterprises can easily validate agent performance in planning and tracking environments before moving into deeper, machine-level automation.

Survey Question #6: Within your manufacturing operation, in which of the following production and supply chain functions are AI Agents currently deployed in production or active pilot?

-

Quality inspection/computer vision (56%): Non-invasive visual QA stands as the baseline operational standard for manufacturing agents. These agents rely on computer vision models to execute real-time analysis of production-line imagery, allowing systems to independently flag anomalies and trigger line halts when defect thresholds are breached.

-

Production scheduling (41%): Organizations are shifting toward self-optimizing supply chains, enabling agents to manage operational planning. These agents dynamically factor demand forecasts, real-time raw material availability, and machine uptime to autonomously adjust floor plans.

-

Robotics & autonomous systems (29%): This data indicates that manufacturing enterprises are moving from digital data processing to physical execution. These agents act as coordination layers, directing robotic arms, Automated Guided Vehicles (AGVs), and cobots.

-

Worker safety monitoring (24%): The lower adoption rate indicates caution among manufacturing enterprises. While these agents are technically mature to track PPE compliance and analyze unsafe behavior via live video feeds, leadership remains hesitant to delegate automated machine shutdowns to an algorithm, keeping safety overrides strictly manual.

-

Energy optimization (19%): The compressed footprint represents a major omission in utility management. Agentic AI can significantly lower operating costs by monitoring consumption, adjusting HVAC loads, and trading power in response to real-time grid pricing signals. But apprehension about potential workflow disruptions keeps this capability stuck in an extended validation phase.

In one of our recent engagements, we worked with a global security provider to deploy an AI-powered computer vision platform for monitoring worker safety and site security across 22,000+ cameras at 180 locations. We automated real-time detection and fed every false alarm back into model retraining, cutting false positives by ~55% and doubling the camera coverage each operator could handle, without adding headcount.

4. Finance

Agentic AI adoption is becoming increasingly function-specific in financial services. The survey data show that organizations are deploying AI agents in workflows that are data-heavy, process-driven, and well-suited to repeatable decision support.

This indicates a shift toward operationalized AI adoption. Financial organizations are focusing on use cases where agents can handle document-heavy processes, assist with rule-based decisions, and improve response speed without requiring broad workflow redesign in the first stage.

The data below maps the finance functions in which Agentic AI is currently deployed across 380 surveyed financial institutions.

Survey Question #7: In which of the following finance functions are AI Agents currently deployed? (Multi-select.)

-

Underwriting (67%): The strongest deployment concentration appears in underwriting, where structured applicant data, credit bureau inputs, banking feeds, and internal risk rules can be evaluated through defined decision models.

-

Customer service chatbots (61%): Transaction-enabled service automation is becoming a major use case in finance. Current deployments support user authentication, account and transaction retrieval, routine service actions, and end-to-end resolution of standard customer requests.

-

Regulatory compliance / RegTech (39%): Compliance-related deployments focus on continuous monitoring, suspicious-pattern detection, audit-trail creation, and regulatory documentation. These use cases show where Agentic AI is being applied to high-volume review processes that require traceability and evidence generation.

-

Document processing and KYC (32%): Verification workflows remain a strong fit for Agentic AI in finance. Organizations are using agents to extract data from identity documents and forms, validate information against sanctions and politically exposed persons lists, and support the completion of KYC workflows.

-

Wealth management (5%): Wealth management shows limited penetration compared with other operational finance functions, suggesting that advisory-heavy workflows still depend heavily on human judgment and relationship context. Current use cases are concentrated around portfolio drift monitoring, rebalancing support, and performance commentary preparation.

“AI is being embedded into the core operating fabric of enterprises”

~ Rajesh Nambiar, President, NASSCOM

03

Looking at the Gap Between Agentic AI and its P&L Impact

We observed that Agentic AI spending has crossed a threshold from cautious experimentation to committed enterprise investment. However, this funding surge raises a sharper question for leadership about the ROI of this investment.

Until now, many boards have approved spending to avoid falling behind competitors. The next phase requires enterprises to measure their operational value and contributions to business outcomes. Throughout this report, "P&L impact" refers to the share of organizations in a sector that reported a measurable effect on profit or loss from their Agentic AI deployments. We asked the following questions to collectively analyze Agentic AI’s P&L impact and budget implications:

Survey Question #8: How is your organization's budget projected to change over the next 12 months compared to the past 12 months?

Survey Question #9: For each Agentic AI outcome level, please indicate whether your organization has achieved the intended ROI to date.

-

42% of Enterprises are Significantly Increasing Agentic AI Investment: Capital is being funneled heavily into software development, technology, and financial services. Our analysis shows these data-rich industries are aggressively backing Agentic AI because their workflows run on deterministic code and strict rule sets. The tech sector sees a 58% P&L impact, while financial services experiences a 34% impact. This hyper-focused spending makes these sectors the primary drivers of high-performing enterprises that achieve truly transformative outcomes with Agentic AI.

-

37% of Enterprises are Moderately Increasing Agentic AI Investment: This phased funding approach is the dominant strategy across healthcare and manufacturing enterprises. These verticals face steep operational hurdles, including physical supply chain complexities, legacy equipment integration, and intense clinical regulatory oversight. Consequently, their budgetary growth is systematic rather than rushed. This steady approach yields a 26% P&L impact in healthcare and an 18% impact in manufacturing, directly fueling organizations reporting significant ROI from their agents.

-

13% of Enterprises are Maintaining Their Investment, While 8% are Decreasing: The combined subset represents the operational baseline for the broader market, where other unclassified industries see an average P&L impact of 14%. This group includes highly regulated utilities, commoditized retail, and distressed media. While these sectors can show strong potential on paper, severe data residency friction, security gaps, and early over-budgeting have temporarily frozen or reduced their spending. These organizations reflect the broader market reality where only some enterprises have achieved a measurable EBIT impact from their investments, while the rest remain stuck trying to right-size their spending to match actual returns.

Enterprises

“The business value is not from that 3% or 5% efficiency gain. It's from rethinking that entire workflow”

~ Andrew Ng, Founder of DeepLearning.AI, Co-founder of Coursera, former Head of Google Brain

04

Closer Look at Barriers Slowing Down Agentic AI Adoption

After mapping Agentic AI adoption across industries, our study examined the barriers limiting enterprise-scale deployment. The results show that adoption is not being slowed by one universal constraint. In fact, each industry faces a distinct barrier profile shaped by its operating environment, data sensitivity, regulatory exposure, system maturity, and tolerance for autonomous decision-making.

This matters because Agentic AI scale cannot be solved through tooling alone. A software company, a bank, a hospital network, and a manufacturer may all deploy AI Agents, but the conditions required to scale them are fundamentally different.

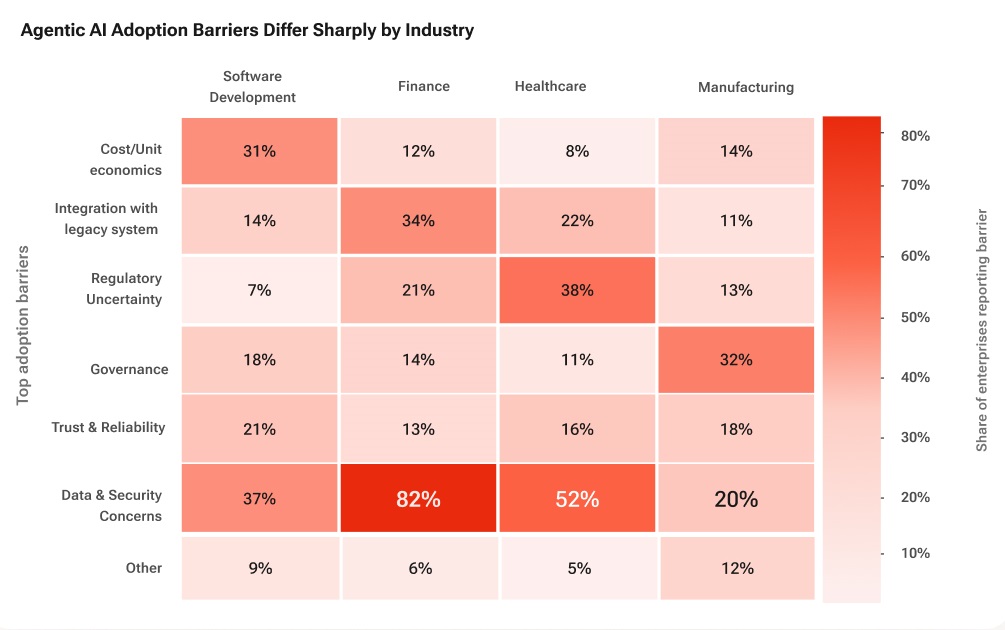

Survey Question #10: Which is the most significant barrier to Agentic AI adoption for your organization?

1. Software Development and Technology: Scale-Economics Problem

Software development shows a different barrier profile. Data and security concerns lead at 37%, but cost/unit economics at 31% is the defining signal. Unlike finance or healthcare, the tech sector is not primarily waiting for any permission to experiment. It is already experimenting heavily. The problem is whether Agentic AI can scale without damaging software margins.

This finding points to the hidden cost of agentic workflows. Continuous code reasoning, testing, debugging, documentation generation, and multi-agent orchestration can increase compute usage, API dependency, review cycles, and infrastructure overhead. At pilot scale, these systems look productive. At production scale, the economics become harder to defend.

Trust and reliability at 21% adds another constraint. Engineering teams can tolerate Agentic AI assistance, but they cannot tolerate unstable outputs inside production engineering pipelines. Therefore, the sector’s next challenge is proving that AI Agents can write/review code, securely and reliably, with a cost structure that supports sustainable deployment. Tech firms must solve the cost-per-token bottleneck before their agent investments turn a true profit.

2. Finance: Security Concerns

Finance reports the highest concentration of severe barriers in our study, with data and security concerns at 82%. It signals that financial organizations are hesitant to let autonomous systems access, interpret, or act on sensitive customer, transaction, credit, and institutional data without strong containment controls. Governance at 34% and regulatory uncertainty at 21% reinforce the same pattern.

Finance leaders are not only concerned about whether AI Agents can perform tasks accurately. They are concerned about whether every agentic action can be controlled, traced, audited, and justified in accordance with strict internal and regulatory standards.

The finding suggests that finance will scale Agentic AI first in workflows where data exposure is limited and decision boundaries are clearly defined. Until AI Agent development companies can guarantee absolute, zero-leakage compliance that satisfies rigid institutional audits, Agentic AI will remain restricted to low-risk back-office tasks rather than high-autonomy use cases such as portfolio management or risk-sensitive decisioning.

3. Healthcare: Data and Liability Threshold

Healthcare shows a dual pressure point, with data and security concerns at 52% and regulatory uncertainty at 38%. This combination indicates that healthcare organizations are evaluating it through the lens of patient privacy, clinical accountability, compliance (such as HIPAA), and the consequences of incorrect or unexplainable outputs. Governance at 22% further shows that healthcare leaders need more than model accuracy before expanding adoption. They need clear oversight models, escalation protocols, audit trails, and defined boundaries between administrative automation and clinical decision support.

Our experts opined on this: healthcare adoption will remain strongest in administrative, documentation, scheduling, engagement, and non-diagnostic workflows. Clinical expansion will be slower because the risk profile changes sharply once agents influence triage, diagnosis, treatment planning, or patient care prioritization.

4. Manufacturing: Integration with Legacy Systems

Manufacturing stands apart from the other sectors because its leading barrier is integration with legacy systems at 32%. This shows that the adoption challenge is grounded in infrastructure. Enterprises are dealing with older equipment, fragmented plant-floor systems, SCADA environments, sensors, ERP platforms, and operational technology that were not designed for autonomous AI workflows.

Data and security, at 20%, and trust and reliability, at 18%, remain relevant concerns but are secondary to the integration problem. In manufacturing, Agentic AI must interact with physical processes, production constraints, machine states, and safety systems. This makes deployment more dependent on system interoperability than on model capability alone.

According to our experts, manufacturing organizations will gradually scale Agentic AI through bounded use cases such as quality inspection, production scheduling, predictive maintenance, and energy monitoring. Deeper autonomy in plant-floor operations will require modernization of data pipelines, machine connectivity, and OT/IT integration.

Multi-select Survey Data. Higher Value indicate stronger barrier intensity

5 Agentic AI Predictions for 2027 Worth Knowing

The data in this report describes a market in motion amid an Agentic AI shift, and the cost of delaying this shift can be very high. Nearly six in ten enterprises have crossed the Agentic AI threshold, yet only 16% have realized a transformative impact. The 5 predictions about the state of Agentic AI in 2027 are based on 1,500 responses from senior executives in four major industries.

1. Agent Count Becomes Part of the Budget

Finance teams will start tracking deployed agents the way they track FTEs. Expect board packs to include agent headcount, cost per task, and productivity-equivalent reporting alongside traditional workforce metrics. The CFO who cannot answer "how many agents are running in production?" will be at the same disadvantage that the CFO who couldn't read a cloud spend chart was in 2019.

2. Performance Gap Widens Before it Narrows

The 16% of high performers identified in this report will likely increase to 25-30% by the end of 2027. Crucial operational prerequisites, including deep workflow redesign, strict data governance, and precise output measurement, yield compounding returns that cannot be rapidly acquired through short-term software purchases. Organizations failing to initiate these structural changes by mid-2026 risk a multi-year operating-model disadvantage that will be increasingly difficult to close.

3. First Major Agentic Incident Forces Binding Governance

Within the next 12 to 18 months, an autonomous agent will fail publicly. The response will be enforceable obligations of existing advisory frameworks, such as NIST AI Risk Management Framework, MeitY's IndiaAI guidelines, and the EU AI Act's high-risk provisions. The enterprises operating without formal agent governance today are not facing a question of best practice; they are facing a closing compliance window.

4. Multi-Agent Orchestration Becomes the Next Platform Battle

The strategic value will shift upward to the orchestration layer, the system that arbitrates which agent handles which workflow, governs handoffs between them, and enforces policy across the stack. The enterprise orchestration platforms will likely consolidate the market by late 2027, with point solutions either absorbed or relegated to specialist use. Selecting an orchestration layer now is, therefore, an architectural commitment.

5. Reliability will become the binding constraint, Not Cost

Per-task agent costs have fallen roughly 10x in 24 months and will continue to decline. By 2027, executives will not ask whether AI agents are affordable but whether they can be trusted at scale. The enterprises that invested early in observability, structured evaluation, and human-in-the-loop design will hold a durable advantage.